As poor as last year was for investors, 2023 has fortunately been a near mirror image. Stocks and bonds have both made solid gains to kick off the new year. The economy is in better shape than most expected, and overall inflation is also coming down, making a very nice combo.

- Stocks have had a huge start to 2023, but a better economy could open the door to continued gains.

- The January employment data show no sign of slowdown.

- The economy does not appear close to a recession.

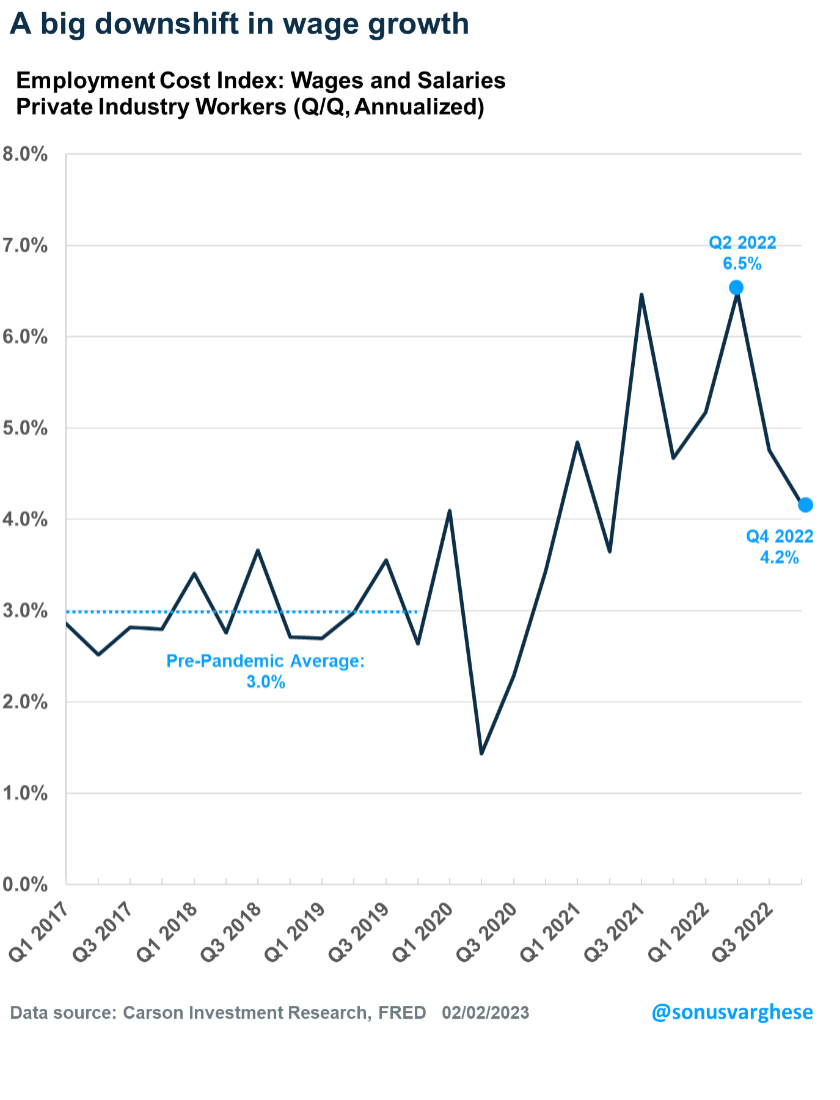

- Wage growth is trending lower, which should be good news for the Fed as it downshifts the pace of rate hikes and closes in on a peak rate.

- A relatively stronger than expected economy means the Fed is likely to keep rates higher for longer.

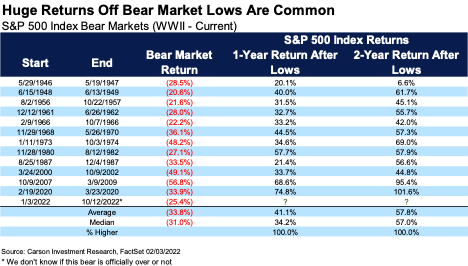

Stocks bottomed in mid-October and have gained as much as 17% off those lows. What could be next? After previous bear market lows, stocks had gained nearly 40% a year later and 60% two years later. Yes, the returns off the October lows have been impressive, but more gains are likely if history is a guide. The stock market’s strength is also a good indicator of economic growth, since stocks lead the economy. In other words, strength in stocks could be the market’s way of sniffing out better economic data. That means we could see a surprisingly strong second half of 2023.

The Labor Market is Defying Recession Forecasts

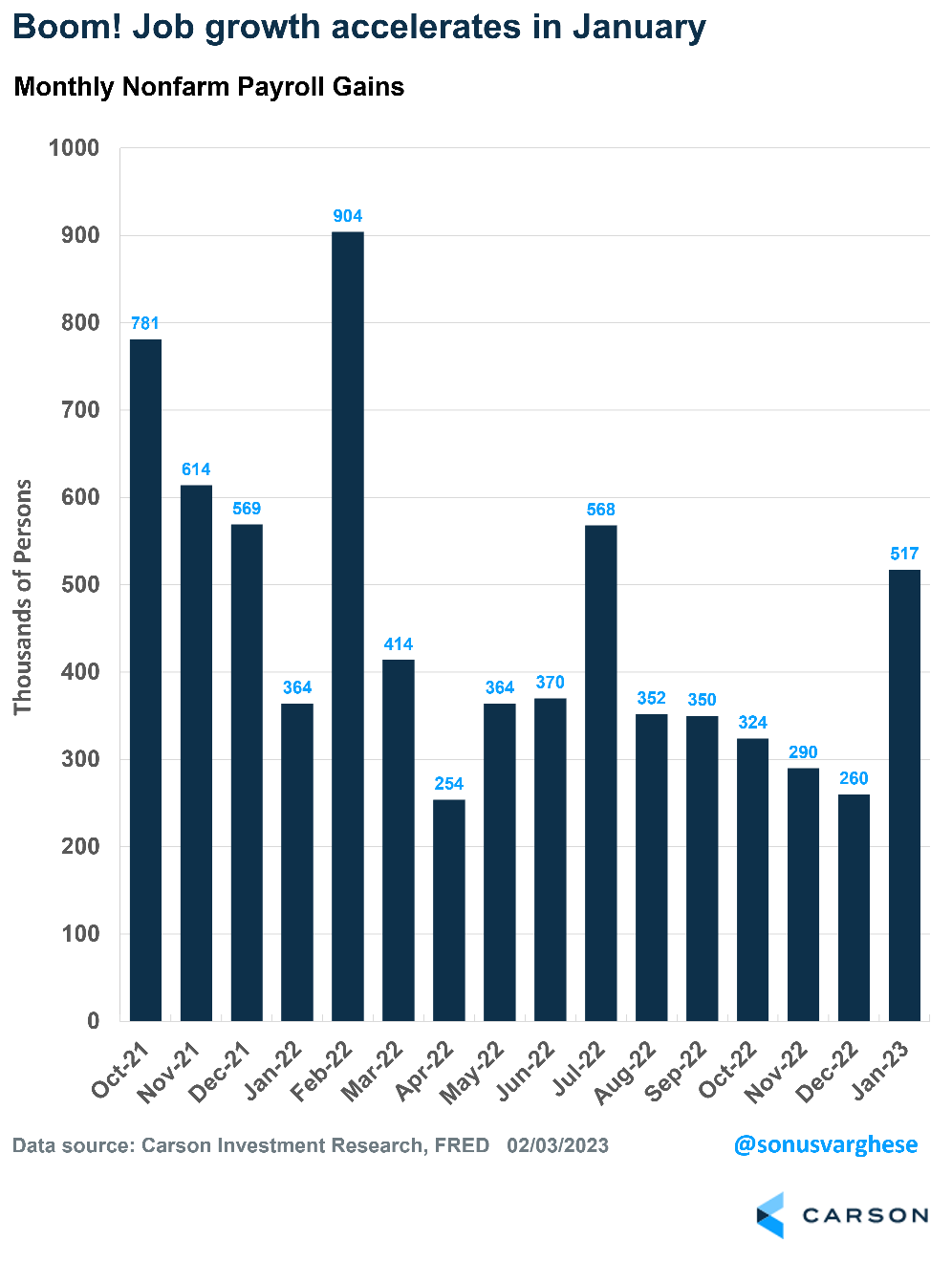

Let’s keep it simple: The economy created 517,000 jobs in January, well above expectations for a slowdown to 175,000.

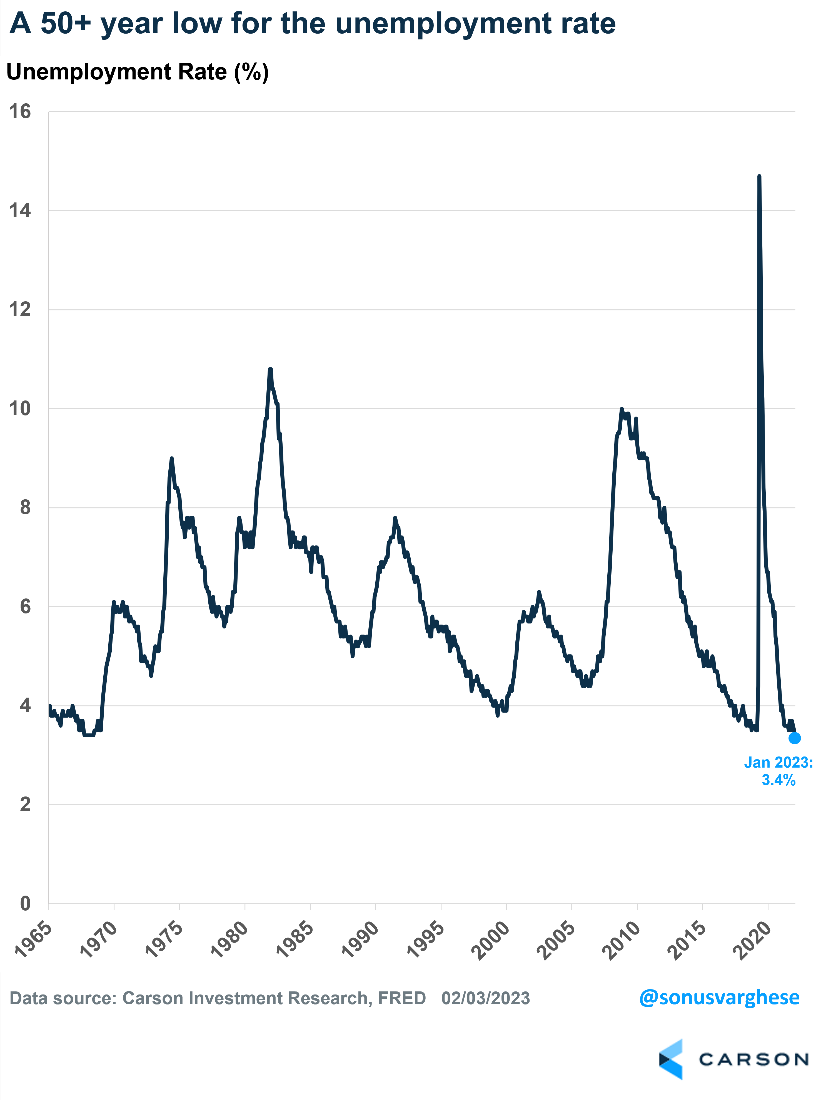

The unemployment rate is 3.4%, the lowest level since May 1969.

It’s like the labor market, i.e., America’s employers, are on a mission to upend forecasts of a recession in 2023.

Also, revisions suggest payroll growth was stronger than we thought in 2022. The Bureau of Labor Statistics now says the economy created 4.8 million jobs in 2022, as opposed to the previous estimate of 4.5 million.

Forget recessions and landings; these numbers suggest an employment boom!

Strong Numbers Under the Hood

The data corroborate what we’ve been seeing in leading employment indicators, such as weekly initial claims for unemployment, which fell to the lowest level in nine months last week. January data typically tend to be quite noisy, due to seasonal effects. But even accounting for that, let’s not miss the big picture, which is that the labor market is very resilient, if not outright on fire.

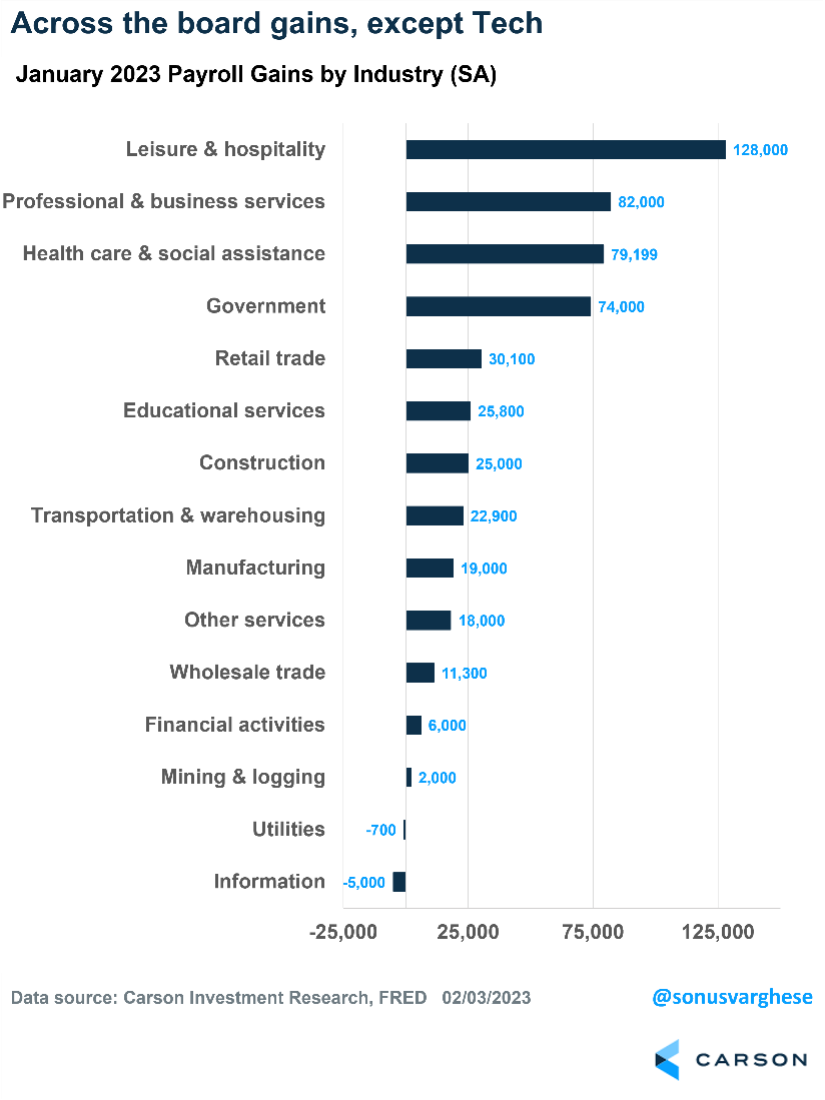

The huge payroll gain in January was not due to outsized gains in one sector either. Cyclical sectors, such as manufacturing, construction, and wholesale/retail trade services, all added a total of 85,000 jobs. That contradicts the narrative of a significant slowdown in these areas.

Meanwhile, the service industry is growing rapidly. Americans are spending, and employers are responding, including by adding 113,000 net jobs across accommodation, restaurants, and bars.

Information processing, which includes technology and utilities, were the only sectors that saw job losses, and not many.

What Does This Mean for Monetary Policy?

The Federal Reserve raised rates by 0.25% last week, taking the federal funds rate to the 4.50-4.75% range. This is the slowest pace of increases since last March and a welcome downshift after the aggressive pace last year.

Fed officials also said ongoing interest rate increases will be appropriate to return inflation to their 2% target over time, suggesting they’re not done with rate increases yet. But the extent of future increases will take the totality of rate hikes so far plus incoming data, which indicates they are close to peak rate, perhaps around 5%.

Mainly, the Fed is waiting to see disinflation in the “core services inflation, ex housing” category. This is closely tied to wage growth, and there’s good news on that front. Wage growth is decelerating. The employment cost index, which is perhaps the most stable measure of wage growth, showed a sharp deceleration in the fourth quarter, corroborating other measures.

The best news is that wage growth is slowing even as the unemployment rate is at 50+ year lows. This is not what textbook theory or forecasters would predict. But we’ll take reality over that. And Fed Chair Jerome Powell’s comments after the Federal Open Market Committee (FOMC) meeting suggest the Fed might be inclined to do the same. In other words, they don’t need to be convinced that inflation is coming down and will remain low only if the unemployment rate surges. They just need to see the data, i.e., continued deceleration in wage growth, and disinflation in core services ex housing.

Of course, stronger economic growth means the Fed is likely to keep interest rates higher for longer, which is contrary to market expectations of rate cuts in the second half of 2023. But we believe the economy is strong enough to handle higher rates currently.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01649284