The past few weeks we’ve advised readers to be on the lookout for seasonal late February/early March weakness. After the 11th best start to a year ever as of Valentine’s Day, some sluggishness was expected. Well, stocks had their worst week of the year last week and are now down three weeks in a row for the first time since December.

- Late February seasonal weakness is right on cue.

- The Fed rate hike path is being repriced higher and is contributing to market volatility.

- Recent payrolls, consumption, income, and inflation data came in hot.

- Better weather and seasonal adjustments are likely causing this slump; we expect things to improve soon.

- Various levels of market support are near, and we don’t expect the weakness to spread much further.

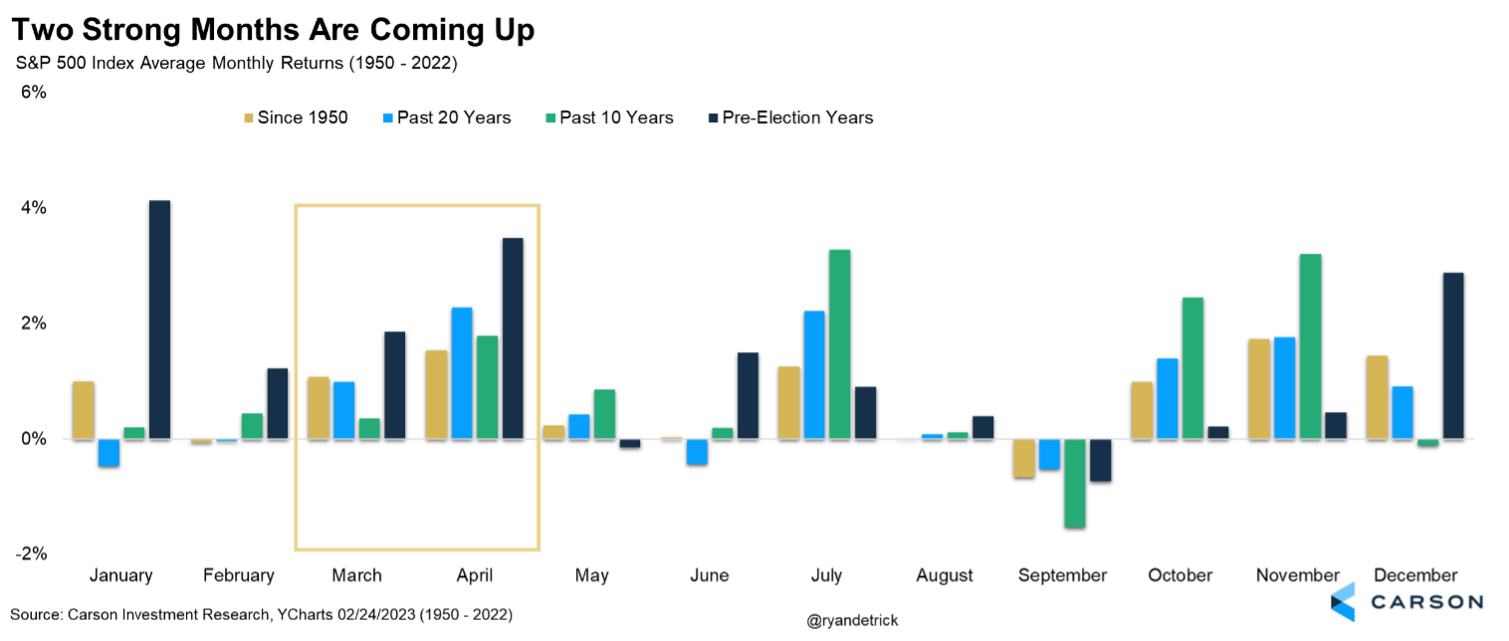

- Year three of a new president is historically strong.

- The economy is still showing no signs of a recession, led by a strong consumer.

The S&P 500 is still 11% above the October lows and we do not anticipate new lows. After nearly a 17% rally into mid-February, this weakness is perfectly normal. February is considered a hangover month, and sure enough, after the fun we had in January, that truism is playing out again.

Here’s the good news: The next two months are typically some of the best of the year and are even better in a pre-election year. We’ve seen signs of consistently bearish sentiment and worry, which is exactly what we want to see for a tradeable bottom to form.

Markets Now Expect Higher Rates for Longer

Volatility has returned to the equity markets. Ironically, this has come amid a slew of stronger than expected economic data, including payrolls and consumption. Consumer confidence is also rising.

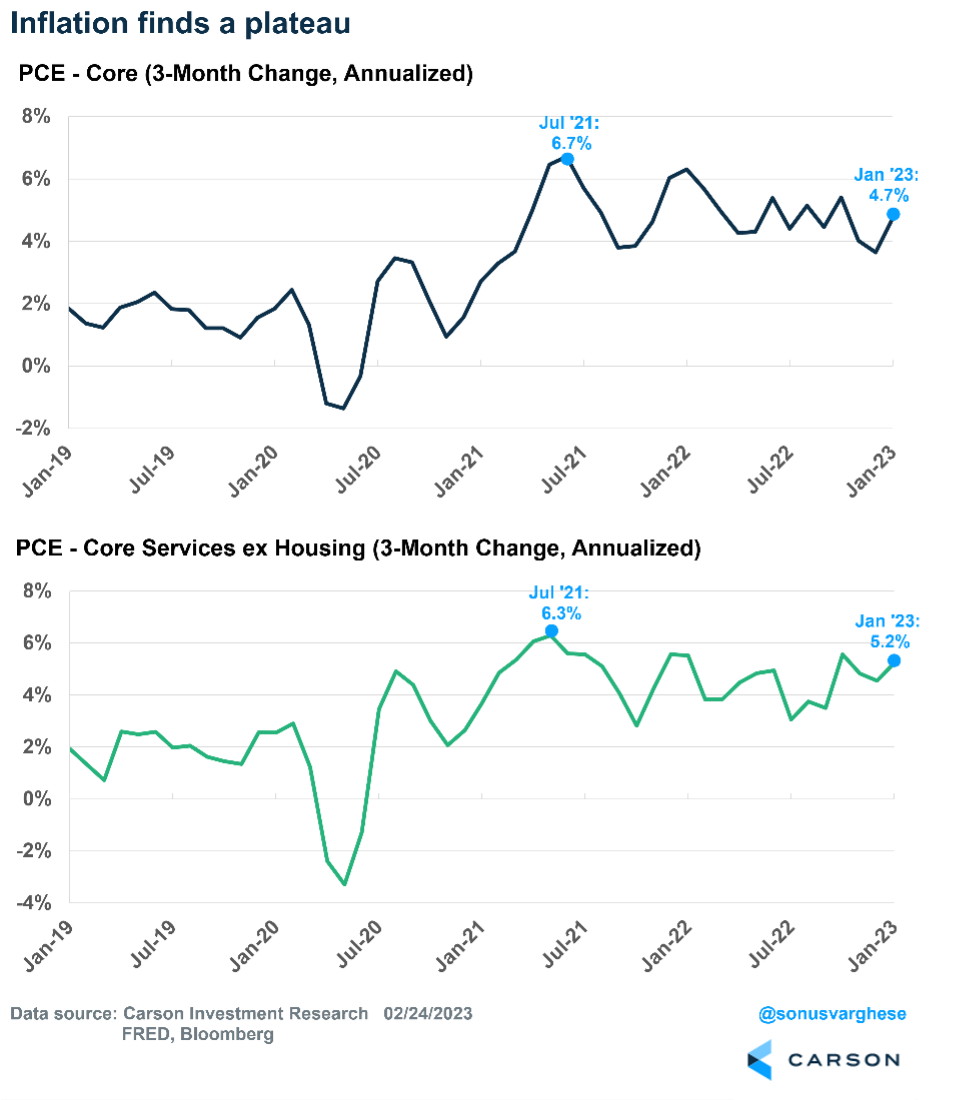

The problem is inflation numbers have stopped decelerating as fast as they were a few months ago. We wrote about this when the January CPI data was released — inflation is much lower than it was last year, but it is still elevated. Part of the reason is a strong economy is putting upward pressure on prices, including discretionary spending, such as eating out, going to movies/concerts, recreational activities, and buying clothes and household goods.

The latest PCE (personal consumption expenditures) inflation data, the Fed’s preferred inflation index, confirms that narrative. Core inflation, which excludes food and energy, has been running at a 4.7% annualized pace over the past three months. That’s down from the peak of 6.7% we saw 18 months ago, but it’s still high. Recently, Federal Reserve Chair Jerome Powell has talked about keeping an eye on core services ex housing inflation as well. That has been running at an annualized pace of 5.2% over the past three months and has more or less plateaued.

Core services, ex housing, tend to be correlated to wage growth, and there is fairly strong evidence that wage growth is decelerating, which should ultimately push core inflation lower.

However, until that actually shows up in the official data, expect the Fed to keep pushing rates higher and keeping them there.

More Uncertainty Around the Fed

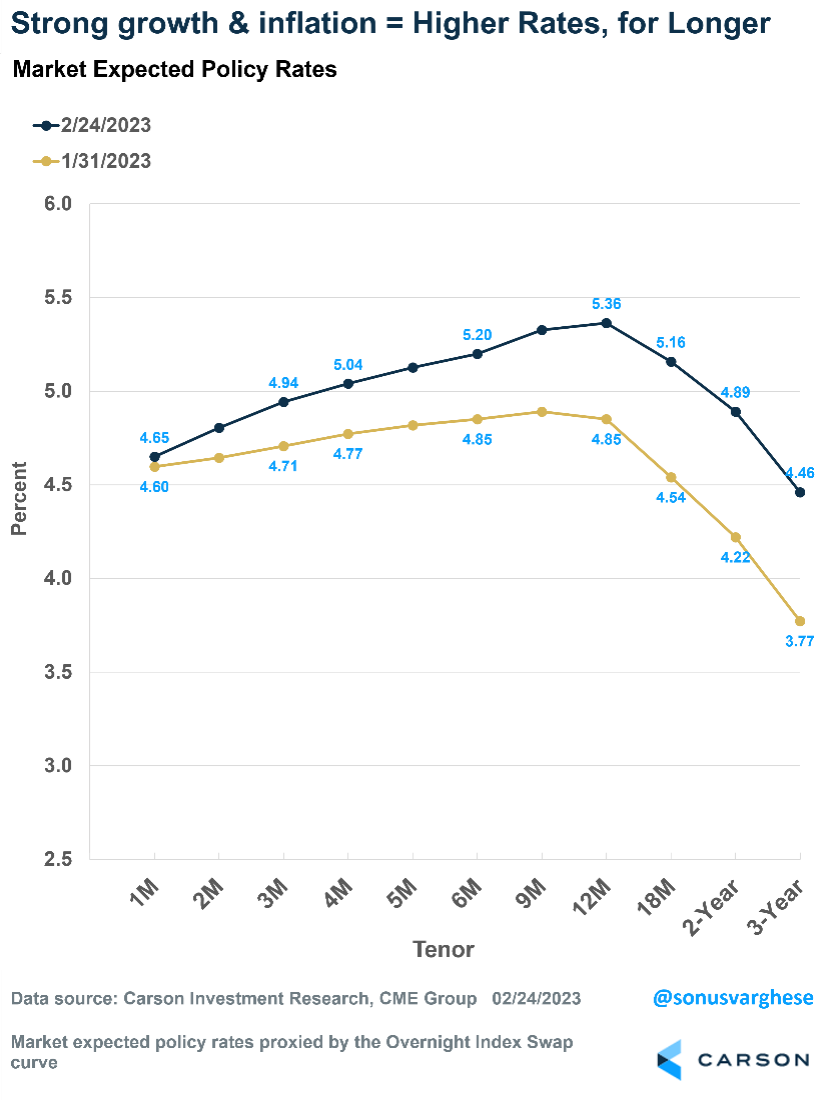

Three weeks is not a very long time, but that’s all it took for investors to move up their interest rate expectations. At the end of January, the expectation was for the Fed to reach a peak rate (for the federal funds rate) of about 4.9% by the end of the year, followed by a series of cuts over the following year.

That’s shifted quite significantly, with markets expecting the “terminal rate” to move as high as 5.36% by the end of this year. That translates to an additional 0.50% of rate hikes this year. The expectation is that the Fed will raise rates by 0.25% over the next three meetings, i.e., March, May, and June. Previously, the expectation was for rate hikes to be done in March.

In fact, there’s even a 27% probability that the Fed raises rates by 0.50% at its March meeting. We think a 0.50% increase is unlikely, but higher market odds reflect uncertainty about what the Fed is going to do, which has added to market volatility.

Also, as the chart above shows, higher rates are expected for longer. Investors now expect the federal funds rate to be above 5% even in June 2024. Three weeks ago, they expected rates to fall to around 4.5% by then.

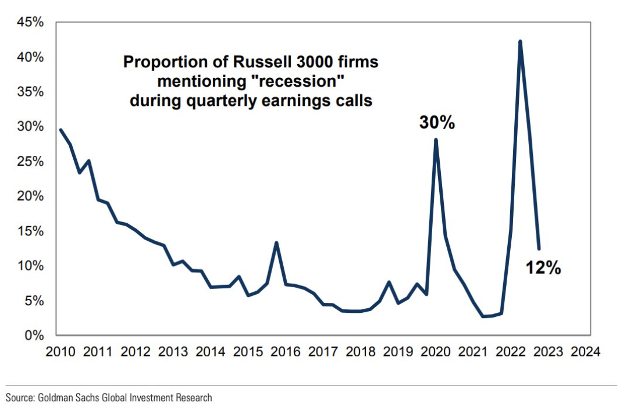

All in all, we’ve gone from a period of apparent consensus on what the terminal rate would be to renewed uncertainty. And that’s happened on the back of firmer core inflation readings and stronger than expected economic data. We’re getting fewer recession calls now — in fact, the proportion of firms mentioning “recession” in quarterly earnings calls has fallen significantly.

We think strong economic data is good news, which will ultimately be reflected in stocks. Wage growth data also indicates inflation will continue decelerating. It just may not happen as quickly as anyone would like, for several reasons, including how official data is measured.

Note that the second half of February has historically been troublesome for stocks, as we have discussed previously. However, two of the strongest months of the cycle are coming up soon.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01670457